Start a new document with this content. Open the editor to build from scratch — paste in what you need and keep writing.

Forming a joint venture checklist

Forming a joint venture (JV) can be a powerful way to expand your business, but it’s essential to ensure that every step is carefully planned and executed. This joint venture checklist guides you through the process, from conducting joint venture due diligence to drafting the joint venture agreement.

Following this due diligence checklist for a joint venture will help you avoid common pitfalls and build a solid foundation for your partnership.

How to use this forming a joint venture checklist

Here’s how to use this joint venture due diligence checklist effectively:

- Follow the process: This checklist walks you through the key phases of setting up a JV, from due diligence to formalizing agreements. Use it to ensure you cover all necessary tasks in your joint venture agreement checklist.

- Customize for your situation: Every JV is unique. Tailor the checklist to meet the specific needs and goals of your venture while ensuring alignment between both parties.

- Stay organized: Keep track of progress by checking off completed tasks in your joint venture checklist and making notes along the way. This will help prevent missed details and ensure thorough preparation.

- Get expert advice: Involve legal, financial, and tax advisors throughout the process to ensure your due diligence for joint venture is comprehensive and your agreements are compliant with regulations.

By following this joint venture checklist, you'll be well-prepared to form a successful and legally sound partnership.

Checklist

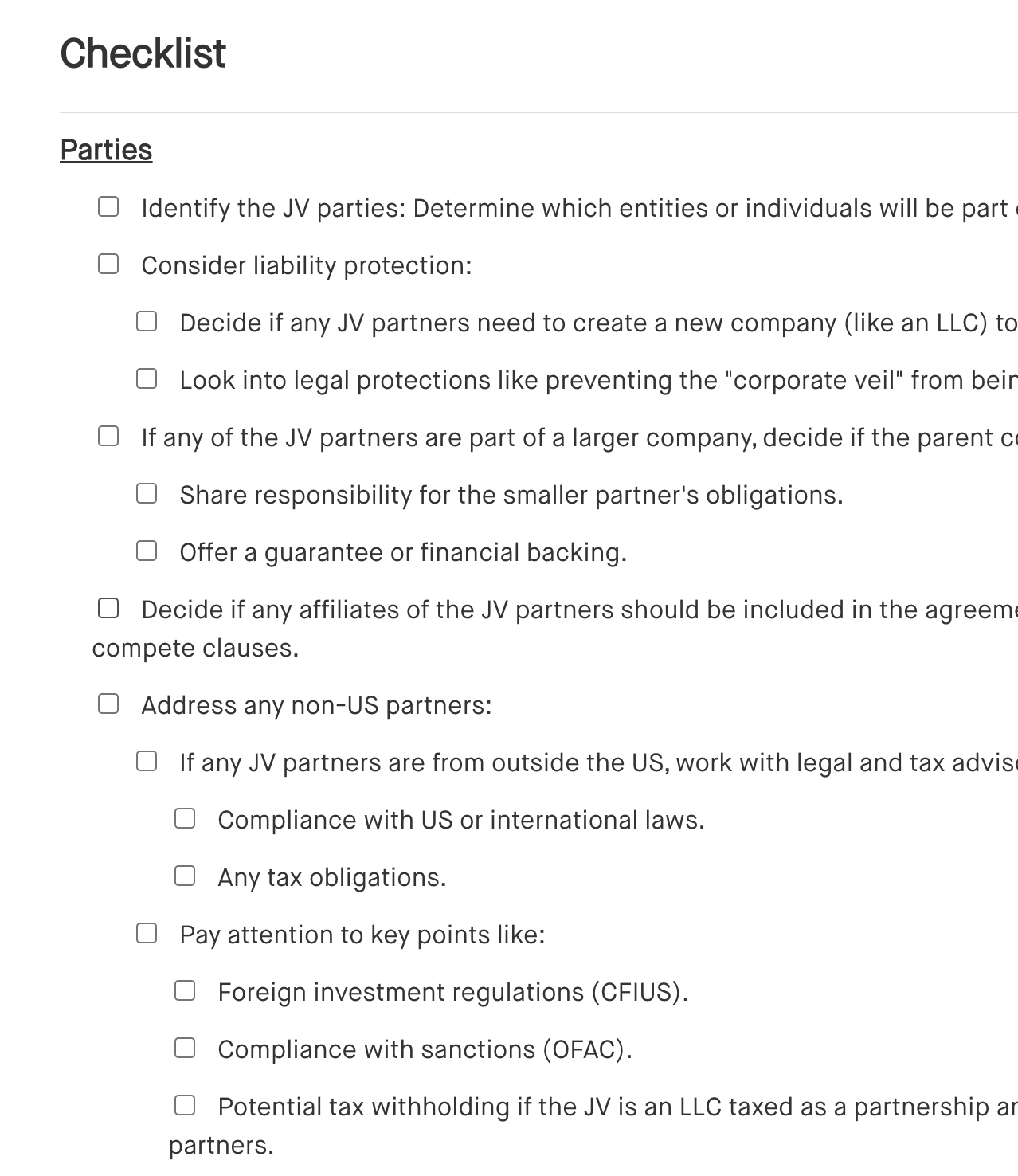

Parties

[ ] Identify the JV parties: Determine which entities or individuals will be part of the joint venture (JV).

[ ] Consider liability protection:

[ ] Decide if any JV partners need to create a new company (like an LLC) to protect themselves from liability.

[ ] Look into legal protections like preventing the "corporate veil" from being broken.

[ ] If any of the JV partners are part of a larger company, decide if the parent company should:

[ ] Share responsibility for the smaller partner's obligations.

[ ] Offer a guarantee or financial backing.

[ ] Decide if any affiliates of the JV partners should be included in the agreement, especially for things like non-compete clauses.

[ ] Address any non-US partners:

[ ] If any JV partners are from outside the US, work with legal and tax advisors to check:

[ ] Compliance with US or international laws.

[ ] Any tax obligations.

[ ] Pay attention to key points like:

[ ] Foreign investment regulations (CFIUS).

[ ] Compliance with sanctions (OFAC).

[ ] Potential tax withholding if the JV is an LLC taxed as a partnership and income is going to non-US partners.

Preliminary documents

[ ] Make sure both parties agree to protect any confidential information before sharing sensitive details about the JV. Use a mutual confidentiality agreement designed specifically for JV discussions.

[ ] Consider a letter of intent or term sheet:

[ ] Establish the basic terms of the JV before investing significant time or money.

[ ] Choose the appropriate letter of intent for either a 50/50 JV or a majority/minority JV structure.

[ ] If exclusivity isn't covered in the letter of intent, think about signing an exclusivity agreement to ensure both parties commit to negotiating solely with each other for a set period.

[ ] If one party is a public company, consider using a standstill agreement to limit the other party’s ability to purchase its stock during negotiations.

[ ] Before negotiating detailed JV terms, work on a comprehensive business plan that includes budgets and cash flow projections. This will guide the JV’s financial strategy for the near future.

Due diligence, consents and approvals

[ ] Conduct thorough due diligence:

[ ] Review both legal and business aspects of the JV, including the business plan and the long-term working relationship between parties.

[ ] Assess cultural fit between prospective JV parties to ensure a smooth partnership over time.

[ ] Consider feasibility studies and market research:

[ ] Evaluate whether a feasibility study or market research is needed to confirm the JV’s business plan and its potential for success.

[ ] Obtain necessary consents and approvals:

[ ] Ensure each JV party knows what internal approvals (from shareholders, lenders, etc.) are required to enter into the JV and plan for obtaining them.

[ ] Check for regulatory filings:

[ ] Identify any required regulatory actions, such as antitrust reviews, CFIUS filings, or industry-specific notifications.

[ ] Determine if the JV formation is reportable under the Hart-Scott-Rodino Antitrust Improvements Act or other relevant laws.

[ ] Prepare for public disclosures:

[ ] Plan for any necessary public announcements or disclosures, especially if one of the JV parties is a public company. Ensure compliance with securities laws and coordinate the timing of announcements.

Purpose and scope

[ ] Decide whether the purpose should be narrowly or broadly defined, considering the types of activities and geographic areas the JV will focus on.

[ ] Determine if any activities or regions should be specifically excluded from the JV’s scope.

[ ] Consider whether the JV’s purpose may need to expand or shift as the business grows.

[ ] Decide if JV party or other approvals will be required for any changes to the original scope or business purpose.

[ ] Determine whether JV parties or their affiliates will be required to present relevant business opportunities (within the JV’s purpose) to the JV.

[ ] Set guidelines for how the JV will decide to pursue or reject presented opportunities.

[ ] Establish if there will be any restrictions on a JV party pursuing an opportunity the JV declines.

Structuring the joint venture

[ ] Determine if the JV will have a fixed or open-ended term. If fixed, consider if there should be a renewal option (e.g., auto-renewal or mutual agreement to extend).

[ ] Choose between a separate entity or direct contract:

[ ] Decide if the JV will be structured through a new entity or via a direct contractual relationship between the parties.

[ ] For simpler JVs, a contract like a collaboration, supply, or distribution agreement may be sufficient.

[ ] For complex or longer-term JVs, a separate entity (e.g., LLC, corporation) might be more suitable.

[ ] If using a separate entity:

[ ] Decide if the entity will be newly created or an existing entity (e.g., a subsidiary of a JV party).

[ ] Choose the type of entity (LLC, corporation, limited partnership, etc.) and the state of formation (Delaware is common for LLCs).

[ ] Consider the JV’s tax and accounting preferences, such as the need for pass-through taxation or control over financial reporting.

[ ] Handle legal formalities:

[ ] Ensure all necessary registrations, licenses, and approvals are in place for the chosen entity.

[ ] Confirm that all equity interests are issued in compliance with federal and state securities laws if relevant.

[ ] For cross-border JVs, account for any foreign legal or US laws that may impact the structure.

[ ] Plan for exits or transfers:

[ ] If parties may want to exit the JV or transfer their interest during its term, build flexibility into the structure, such as buy-out provisions or transfer rules.

[ ] Consider restrictions on transferring interests and what consents are required.

[ ] Financing considerations:

[ ] If third-party debt financing is needed, discuss lender preferences regarding the JV’s structure.

[ ] For JVs that may go public in the future, ensure compliance with securities laws and stock exchange requirements.

Equity structure and financing

[ ] Determine funding contributions:

[ ] Decide the proportion of initial contributions or funding each JV party will provide.

[ ] Ensure ownership percentages align with each party's contribution.

[ ] If using a separate JV entity, decide on the capital structure, including:

[ ] Whether there will be one or multiple classes of equity.

[ ] The allocation of ownership, typically proportional to contributions.

[ ] Preferences for different equity classes (e.g., distribution or liquidation preferences, dividends, or interest on invested capital).

[ ] Whether a non-voting or special equity class should be created (e.g., for employee incentive programs).

[ ] Consider the benefits of funding the JV through debt versus equity (tax advantages, etc.).

[ ] Plans for future funding needs:

[ ] Determine if the JV will require additional funding during its term (e.g., for working capital, covering losses, or expansion).

[ ] Consider the impact of third-party investments on the JV’s structure and whether new investors might need special rights (e.g., board seats, anti-dilution protection, liquidation preferences).

[ ] Confirm availability of third-party financing:

[ ] Ensure debt or other financing options are available on acceptable terms.

[ ] Determine if lenders will require collateral or guarantees from JV parties or their affiliates.

[ ] For JVs without a separate entity:

[ ] Define the method for distributing revenues or profits to JV parties.

[ ] If using a profit-based formula, outline the expenses that will be deducted when calculating profits.

[ ] Address how related-party payments (non-arm’s length) will be monitored or adjusted.

[ ] Address tax implications:

[ ] Plan for how payments to JV parties (e.g., dividends, interest, or IP royalties) will be taxed.

[ ] Consult with tax advisors on the taxation of distributions and other payments to ensure compliance with applicable laws.

Contributions

[ ] Clarify what each party is contributing, in particular identify whether contributions will be in cash, assets, or services, and ensure each party’s input is clearly documented.

[ ] Plan for future contributions—if any party is required to contribute more capital in the future, make sure the terms are clear, including what happens if someone doesn't contribute.

[ ] With respect to property contributions:

[ ] Describe the assets being contributed clearly to avoid confusion.

[ ] Confirm the contributing party owns the assets without any legal issues (e.g., liens).

[ ] Determine if the contributing party retains any rights to use the assets after contributing them.

[ ] Consider hiring an independent appraiser if asset value is uncertain.

[ ] Decide if the contributing party should guarantee the condition of the assets.

[ ] If an operating business is being contributed, consider a process to adjust the contribution based on actual performance.

[ ] Determine if the contributing party has a right to repurchase the assets if the JV dissolves.

[ ] Managing liabilities:

[ ] Decide if the JV will take on any liabilities along with contributed assets, and how those liabilities will be shared among the parties.

[ ] Plan for any future or potential liabilities the JV might face.

[ ] Co-ordinate timing and approvals:

[ ] Decide if all contributions will be made when the JV is formed or if some will come later.

[ ] Ensure you have any necessary regulatory approvals or consents from third parties (e.g., landlords, licensors).

[ ] If contributions are made after the JV starts, consider making certain contributions a condition for future obligations.

Intellectual property

[ ] Identify and value intellectual property (IP) contributions:

[ ] Determine any IP rights being contributed to the JV in exchange for equity or other compensation.

[ ] Make sure the value of the IP is clearly assessed.

[ ] If IP is being licensed to the JV:

[ ] Define the limits of the IP’s use (e.g., field of use or geographic restrictions).

[ ] Decide if the license will be exclusive or non-exclusive, and set any limits on exclusivity.

[ ] Specify royalty or payment obligations for the license.

[ ] Determine under what circumstances the license can be terminated, including if a party exits the JV or the JV is sold.

[ ] Outline indemnification obligations for third-party claims like infringement or product liability, including any limits or caps.

[ ] Assign responsibility for IP maintenance (e.g., renewals or updates).

[ ] Clarify ownership of improvements, enhancements, or derivative works developed from the licensed IP.

[ ] Decide if the JV can sub-license the IP, and set limits on the use and ownership of any improvements by sub-licensees.

[ ] Determine who owns new IP developed by the JV and if the JV parties or affiliates will have any licenses to use it, along with payment terms.

[ ] Decide who will handle the production and distribution of the JV’s IP and whether JV parties will be compensated for these services.

[ ] Set clear policies on how JV parties can access or use confidential information, know-how, and other IP belonging to the JV, and establish contractual protections.

[ ] Plan how to manage the JV’s IP if a party exits or the JV ends, and decide if IP rights will differ depending on the circumstances (e.g., if the JV is dissolved or sold to a third party).

Governance and checklist

[ ] Decide how the JV will be managed:

[ ] Determine if the JV will have a board-managed structure or be managed by members, a managing member, or managers.

[ ] Determine if the JV will have a board-managed structure or be managed by members, a managing member, or managers.

[ ] With respect to the board of directors/managers (if applicable):

[ ] Set the board’s size and composition.

[ ] Decide how many board members each JV party can appoint.

[ ] Determine if there will be independent or at-large board members.

[ ] Establish meeting frequency, notice, quorum, and voting rules.

[ ] Decide if board committees are needed, their roles, and authority.

[ ] Plan for board members losing rights (e.g., if a party defaults or dilutes its ownership).

[ ] Include deadlock resolution provisions if there’s a risk of a board impasse.

[ ] Managing member or member-managed JV (for LLCs without a board):

[ ] Determine if the JV will be managed by a managing member, or if all members will take part in management.

[ ] Decide if any matters require approval or notification of JV parties in their roles as equity holders.

[ ] With respect to officers and committees:

[ ] Consider if the JV will have officers, their titles, reporting structure, and authority.

[ ] Decide if technical, advisory, or other committees will be formed, their roles, authority (advisory vs. binding), and member appointment rights.

[ ] Set rules for committee meetings, quorum, and voting.

[ ] Budgeting process:

[ ] Decide who will prepare the JV’s budget and by what date.

[ ] Establish how the budget will be approved and what happens if parties fail to agree on it.

[ ] Determine if any board or committee members, or advisors, will be entitled to fees or expense reimbursements paid by the JV, and set terms for these payments.

[ ] Set the JV’s policy for distributing cash flow or dividends, including how often and how distribution decisions are made.

[ ] Indemnification:

[ ] Define the JV’s indemnification obligations for its directors, managers, officers, or other key figures.

[ ] Set any advancement obligations related to legal or other liabilities.

[ ] Public company governance (if applicable):

[ ] If the JV plans to go public, ensure appropriate governance arrangements for a public company are in place.

Minority protections

[ ] If a JV party holds a minority or non-controlling interest, decide whether they will have any veto or approval rights.

[ ] Define the list of actions that require minority approval.

[ ] Set voting percentages or approval thresholds for these decisions.

[ ] Decide if regular meetings for JV parties are necessary and, if so, establish their frequency.

[ ] Define procedures for calling special meetings, quorum, and voting requirements.

[ ] For any future financing needs, determine if minority JV parties will have a preemptive right to purchase their proportional share of new equity or debt.

Restrictive covenants

[ ] Non-compete and non-solicitation agreements:

[ ] Decide if JV parties will be bound by any non-competition or non-solicitation agreements (for employees or customers).

[ ] Set the time periods for these restrictions, including if they apply after a JV party exits or after the JV is terminated or sold.

[ ] Determine if any restrictions should extend to the JV parties’ affiliates and, if so, identify which affiliates will be affected.

[ ] Assess whether the JV should be restricted from entering agreements with competitors of a JV party or its affiliates.

[ ] Use of names and trademarks:

[ ] Establish any restrictions on the JV using the JV parties’ or affiliates' names and trademarks.

[ ] Consider if these restrictions will still apply after a JV party exits or after the JV is terminated.

[ ] Ensure that the restrictive covenants comply with relevant laws, including enforceability and potential antitrust concerns.

Dispute resolution and deadlock

[ ] Decide how disputes will be handled. You can either:

[ ] Leave the JV agreement silent and resolve disputes through litigation, if necessary.

[ ] Refer disputes to an external expert or neutral third party.

[ ] Opt for third-party mediation to resolve issues.

[ ] Choose third-party arbitration, possibly limited to specific types of disputes.

[ ] Plan for deadlocks (in 50/50 JVs or other situations prone to deadlock) and consider mechanisms to resolve them, such as:

[ ] Consulting independent directors or managers, if applicable.

[ ] Using an external expert, mediator, or arbitrator to break the deadlock.

[ ] Escalating the issue to senior executives of the JV parties for resolution.

[ ] Allowing a JV party to force the termination or winding up of the JV.

[ ] Initiating an auction process to sell the JV to a third party.

[ ] Implementing a buy-sell agreement or put/call options where one JV party can buy or sell equity from the other party.

[ ] Define what types of deadlocks will activate the deadlock remedy (e.g., fundamental issues like business purpose or major financial decisions).

[ ] Determine governing law, venue, and forum for dispute resolution to ensure clarity.

Defaults, exits and termination

[ ] Decide if the JV agreement will include specific remedies for when a party breaches or defaults. Consider default remedies, such as:

[ ] A call right: The JV or non-defaulting party can force the defaulting party to sell its interest, potentially at a discount.

[ ] A put right: The non-defaulting party can require the defaulting party to buy its interest at fair value or higher.

[ ] Suspension or loss of the defaulting party’s rights, such as board appointments, voting rights, or distributions.

[ ] Dilution of the defaulting party’s ownership.

[ ] Dissolution of the JV entirely.

[ ] Determine procedures for defaults, such as:

[ ] Outline the notice requirements before exercising a remedy.

[ ] Define any cure periods for the defaulting party to resolve the breach.

[ ] Specify who has the authority to declare a default or enforce remedies.

[ ] Consider other events that could lead to termination, such as:

[ ] Reaching a fixed end date or failing to meet key performance targets.

[ ] Giving a party the right to dissolve the JV or force a sale of interests.

[ ] Decide which responsibilities will continue after exit or termination (e.g., confidentiality, restrictive covenants).

[ ] Consider if any JV party will need a license for the JV’s IP after termination and on what terms.

[ ] Plan for the dissolution process, including asset disposition, IP allocation, and handling of books and records.

[ ] Be mindful of any regulatory or legal requirements affecting the dissolution process, such as antitrust or foreign ownership rules.

Financial reporting

[ ] Determine what financial statements, tax reports, and other documents the JV must provide to the JV parties.

[ ] Set the reporting frequency (e.g., quarterly, annually).

[ ] Ensure confidentiality is maintained, with clear limits on who can access and share the information.

[ ] Consider how the JV parties’ ownership percentages or control might affect how they report their JV interests (e.g., full consolidation vs. equity accounting).

[ ] Decide on the JV's accounting policies, and ensure they align with or consider the reporting needs of the JV parties.

[ ] Assess if audited financial statements are necessary and, if so, select an auditor for the JV.

[ ] Agree on the fiscal year the JV will use, ensuring it aligns with the parties’ needs where possible.

Employees

[ ] Assess whether the JV requires employees and where they will come from.

[ ] If transferring employees from a JV party’s existing business, check if any changes to their employment terms are needed.

[ ] Decide if the JV or one of the JV parties will be the primary employer.

[ ] Consider if the JV parties or JV will be regarded as joint employers.

[ ] If employees will be shared or seconded to the JV, outline the terms of the arrangement (e.g., secondment agreements).

[ ] Clarify how liabilities for seconded employees will be split among the JV parties.

[ ] Ensure the JV complies with federal, state, and local labor laws, including workers’ compensation and unemployment insurance.

[ ] Decide if JV employees will be covered under a JV party’s existing benefits plan or if the JV must create its own.

[ ] Assess whether employees need to sign confidentiality, non-compete, or non-solicit agreements with the JV or its parties.

[ ] If equity incentives are planned for JV management, consider creating a separate class of non-voting equity or profits interests.

[ ] Determine whether the JV, a JV party, or a third-party service provider will handle HR functions (payroll, benefits).

[ ] If any JV parties need to terminate employees due to the JV’s formation, decide who is responsible for severance and other termination liabilities.

[ ] Consider WARN Act or state mini-WARN law obligations for layoffs.

Additional entity formation and administrative matters

[ ] If the JV is a separate entity, consider if it might need to report beneficial ownership info to FinCEN under the Corporate Transparency Act (CTA).

[ ] Ensure compliance with any future reporting obligations.

[ ] Confirm the JV’s name is available for use in relevant jurisdictions.

[ ] Check for potential trademark or domain name conflicts.

[ ] Determine the location of the JV’s registered and primary offices.

[ ] Identify where the JV must register to conduct business and file any necessary state forms.

[ ] Allocate responsibility for maintaining the JV’s books and records.

[ ] Decide if the JV will have a website.

[ ] Address the use of JV party names or trademarks on the site.

[ ] Prepare legal documents like privacy policies and terms of use.

[ ] Establish the JV’s cash management policies and bank accounts.

[ ] Determine who has signing authority for bank accounts.

[ ] Assign responsibility for getting a Taxpayer ID for the JV.

[ ] Decide who will file tax returns and handle partnership representative duties if the JV is a pass-through entity.

[ ] Consider if tax distributions will be made to JV parties.

[ ] Identify required insurance policies for the JV.

[ ] Decide if the JV parties should be additional insureds on any JV policies or vice versa.

[ ] Evaluate the need for directors and officers (D&O) insurance, especially for board-managed JVs.

Benefits of using a forming a joint venture checklist

Using a joint venture checklist ensures that you take a structured approach when creating your partnership. Here’s why it’s helpful:

- Avoid missed steps: The checklist helps you stay organized and ensures that no crucial steps in the due diligence joint venture checklist are overlooked.

- Reduce risks: By following the joint venture agreement checklist, you can minimize legal, financial, and operational risks that may arise during the formation process.

- Save time: With everything laid out in this joint venture due diligence checklist, you can work efficiently and avoid wasting time on unnecessary back-and-forths.

- Increase transparency: A checklist ensures both parties have clarity on their roles and responsibilities, promoting smoother negotiations and a stronger partnership.

Frequently asked questions (FAQs)

Outlines guidelines for employee use of social media, including setting clear boundaries, monitoring activity, and ensuring alignment with company values and policies.

Outlines key components for drafting an executive employment agreement, including compensation, benefits, responsibilities, and termination terms.

Details the critical steps to take in response to a data breach, including notification, investigation, containment, and implementing corrective actions.